The decarbonisation of buildings has a vital role to play in responding to the climate emergency.

The decarbonisation of buildings has a vital role to play in responding to the climate emergency.

Buildings are currently responsible for 39% of global carbon emissions. The global building stock is expected to double by 2050 and given that buildings are expected to deliver more and more in terms of comfort, convenience and entertainment, emissions will increase considerably if more is not done to reduce carbon intensity.

According to the landmark report from the UN Intergovernmental Panel on Climate Change, buildings will need to reduce carbon emissions associated with their construction, use and deconstruction by 80-90% by 2050 in order to put the world on a path to limit global warming below 1.5 ºC.

This requires, at minimum, a 3-4% annual rate of deep energy efficiency retrofits and nearly zero energy buildings for all new construction, starting from today. Despite efforts to promote energy efficiency in buildings, the average deep retrofit rate across the EU28 stands at just 1%.

In EBRD's countries of operation, this rate is far lower and nearly zero energy buildings account for less than 0.01% of overall new supply.

This requires a radical transition using a wide variety of business models and tools, as well as significant financial support for market segments affected by complex sets of market barriers.

With experience across the whole building value chain, the EBRD is well-placed to help drive this transition. Since 2006, EBRD has invested EUR 3.8 billion in retrofitting buildings and EUR 1.9 billion in increasing resource efficiency, and reducing emissions and waste in energy-intensive industries in building supply chains.

To deliver these results, the EBRD has applied its unique business model combining policy dialogue, technical assistance and financing in partnership with important stakeholders such as the European Commission, the donor community, global professional associations, co-financiers and policy makers in our countries of operation.

EBRD estimates investment needs for building sector decarbonisation across its countries of operation at between EUR 15,000 and EUR 20,000 billion by 2050. These amounts go far beyond what national governments can provide so the private sector will have to play a key role.

Approaches to supporting investments in green new builds are worthy of an article in themselves. Here, however, we would like to focus on opportunities for scaling up private and public investment in renovating existing building stocks. They include effective ways to address barriers and identifying market drivers for making the climate agenda more of a priority for the sector.

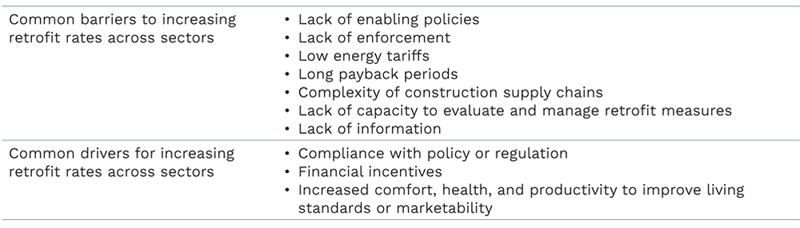

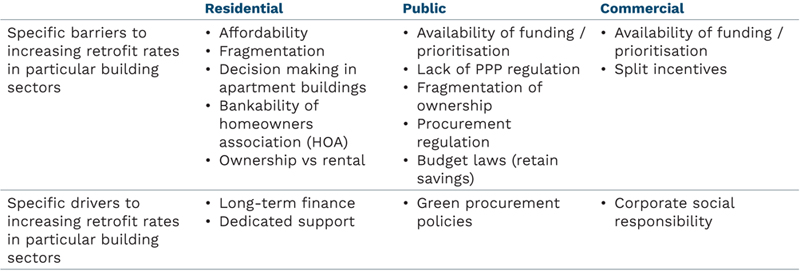

Buildings ownership is highly fragmented but can be grouped into three market segments: residential, public, and commercial. Each faces some common and very specific barriers, as outlined in the tables below.

While it is relatively easy to identify cost-effective decarbonisation actions that will deliver the desired level of climate ambition, accessing the financial resources, securing private sector buy-in and developing the value chains necessary to implement them, remains challenging for a number of reasons.

Deep energy efficiency retrofits often require significant investments in structural and fit out measures that can take as long as 15-20 years to pay back. The high up-front costs and the lack of technical knowledge required to assess and define the technical scope for renovation combined with other pressing needs result in building owners deferring these kind of investments or performing light or sub-optimal renovations.

In multi-apartment buildings, this is further complicated by the number of homeowners involved in decision making processes and the limited ability of homeowners associations to access convenient long-term finance.

These difficulties are further compounded by financing institutions’ lack of understanding of the additional benefits that a deep retrofit can deliver to residential, commercial or public clients. A low-carbon building is a future-proof asset, with higher value and lower operating costs that typically provides a healthier and more productive environment for its occupants.

Transforming the sector requires an integrated and systemic approach. It should combine incentives, education of building owners and financial intermediaries, long-term finance with the establishment of a one-stop-shops providing guidance on what measures to undertake and how to access financial support, adhere with relevant standards, and manage the paperwork throughout the renovation process.

Demand-side actors, including landlords, investors and developers, also need to work together with their counterparts across the value chain, including contractors, materials manufacturers, architects, and facility managers, to address the fragmented nature of the buildings sector and specific market barriers.

These changes would require relevant policy and regulatory reforms to create an enabling environment that can support the transition tailoring the approach to each building category based on the specific barriers and drivers outlined in the table above. More significant financial support is required for market segments affected by complex set of market barriers (i.e. public buildings, rented or social housing, etc.).

At present, EBRD is piloting a number of sector-specific policy initiatives (decarbonisation roadmaps, long term renovation strategies, introduction of enabling legislation), which will form the foundation of a number of innovative financing platforms.

These platforms will use our established network and accumulated experience to facilitate matchmaking between investors, donors and the demand side while aggregating and mainstreaming groups of projects in order to achieve scale in the otherwise fragmented building sector.

We are confident about the success of such approach, because we will do it in cooperation with key European partners and by mobilising capacity of all the major market players in the region.

EBRD's longstanding experience in buildings has seen it invest €3.8 billion in retrofitting buildings and €1.9 billion in increasing resource efficiency, and reducing emissions and waste in energy-intensive industries in building supply chains since 2006.

This has delivered an estimated 14.3 million tonnes of CO2eq reduction annually in emissions reductions across our countries of operation.

For more information and to discuss cooperation, please contact:

Remon Zakaria

Tel: +44 207 338 6000

Email: ZakariaR@ebrd.com